A FRIEND related how he purchased a third-floor shop lot in Selangor for

RM10,000 in late-July. The developer price for the shoplot was about

RM43,000.

He also mentioned another investor who bought an apartment unit in

another area in Selangor for about RM27,000.

“He lives in the same block, having bought his unit earlier for about

RM60,000 from the developer. He made the purchase because he already has a

ready tenant,” he says.

Two things tie these cases together. Both were bought at the same auction

in locations that real estate agents would consider less than ideal. But

both men were thrilled with their bargains as they would have been hard

pressed to find a contractor to build the properties at their purchase

prices.

Says Henry Butcher Marketing Sdn Bhd chief operating officer Tang Chee

Meng: “Some of these locations may not be popular today and the buyers made

the decision in anticipation of future potential. They have a lot of cushion

to ride out the time line.”

Property investment is an adventure. There are gainers and losers. While

the two cases mentioned above are happy with what they consider to be real

bargains, there are those who have lost life savings on such decisions.

“Be clear about your objectives. Is it for your own occupation or an

investment? Or both? Is it for the children? Who is the developer? Is it

accessible? Can you afford it?” says Tang.

Except for some really savvy purchasers, some potential buyers would like

to use property as a hedge against inflation. But they are unable to form

any semblance of a wish list. Developers will always want to make a profit

and sell what the buyer may not need.

Buy undervalued properties, eg at auctions.

“How a development turns out depends very much on developers. Those

conscious about quality and their customers, will command a higher price

compared to those who just build,” Tang says.

Today’s housing needs are no longer production driven. You need to give

the buyer some margin for profit.

Choosing the right location

- Proximity to good schools, shopping and other amenities

- Proximity to parents, children and friends

- Proximity to work place and degree of traffic congestion

- Proximity to healthcare facilities

- Availability of public transport

- Quality of neighbourhood, image, security and flood incidents

Areas popular with expatriates usually fetch better rentals and therefore

higher yields

Established areas fetch better rentals, offer good potential for capital

growth but are more pricey

New growth centres are cheaper, fetch lower rentals, may offer strong

capital growth but carry high risk.

A young person’s choice will be different from his parents’. Developers

have moved from selling a house to marketing a lifestyle or concept.

Although lifestyle is a buzzword today, there are some selection criteria.

Selecting the right property

- Landed vs strata, number of storeys

- Gated and guarded vs conventional

- Personal requirements: space, number of rooms, intermediate vs corner

- Design: layout, facade, facilities

- Developer’s reputation and track record

- Freehold vs leasehold

- Orientation: city living vs suburbs, hill, park, golf course

- Surroundings: is there an oxidation pond or TNB pylons nearby

“Shop around. Look at as many properties as possible to find the one that

best suits you; this is after all your biggest financial investment for some

time to come,” says Tang.

A couple of years ago, there was a great pull towards one particular

established area in Petaling Jaya. There still is. The houses are about 20

years old and prices are still creeping up. The drawback is these houses

need new plumbing and electrical systems. Do you want all that hassle or

would you rather begin anew? Can you wait two to three years?

Completed compared with off-the-plan

The advantage of buying from the developer is that it is new and has

never been occupied before. These are usually cheaper than completed

properties. There is also the defect liability period available, if it is a

residential property.

There is, however, the risk of abandoned projects. One cannot inspect it

before purchase, and there is no certainty of quality or workmanship, which

prompts some buyers to opt for a reputable developer. Most show units are

beautifully constructed; the real thing may be a different story.

You will also have no idea who your neighbours are before buying and

there is always that initial teething problems with defects.

Says Bukit Kiara Properties Sdn Bhd managing director N.K. Tong: “No

matter how strict a developer is with quality, especially with high-end

housing, the buyer will have a slightly higher demand. A developer can react

in two ways: take it or leave it, or give it priority.”

The advantage of buying completed property is you can inspect the house

and its neighbourhood. There is no risk of the project being abandoned; some

buyers would rather pay the extra premium.

The disadvantage is that such properties have been lived in before, and

may have some undesirable history. The other option is to buy a place which

has not been issued its Certificate of Fitness.

Some buyers prefer to buy land and build their own home. While one can

design the place according to one’s requirements, this route will be

time-consuming and comes with a lot of hassle. One will have to deal with

the local authorities, architects, consultants and contractors, to name a

few.

The retirement home

Anticipate your future needs as a senior citizen; consider your physical

needs and financial position. Do not wait until age affects your borrowing

capacity.

“If one is buying for occupation, one will want to be in a location close

to children or friends, or health care facilities and shops. Avoid high

traffic areas. If possible, opt for an area that is pedestrian friendly,”

says Tang.

If it is more than one storey, ensure that the ground floor has a

decent-sized bedroom with bath and toilet facilities. Avoid properties that

have too many split-levels with staircases.

The Boustead group, when promoting Surian Condominium in Mutiara

Damansara, highlighted that its lifts were big enough to fit stretchers.

Another developer of a high-rise condominium in the KLCC area promoted its

handicap friendly facilities.

Consider a garden, which allows one to have some leisure pursuits, or a

condominium with low impact recreational facilities.

It is preferable to stay in a place with security. Tang says some have

bought into the gated and guarded concept in the hope that this concept will

enjoy a better capital appreciation in the long term. “Only time will tell,”

says Tang.

Some development, both landed and high-rise, come with panic buttons. Opt

for a size which is manageable.

Investment compared with own occupation

Choose a location that is rentable and properties that can be easily

sold.

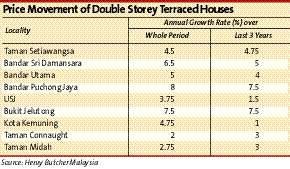

Generally, terraced houses performed well in terms of average capital

growth in Selangor while detached houses are more popular in Kuala Lumpur.

Terrace houses are also less volatile compared to semi-detached and detached

houses, which register bigger declines during economic downturns, says

Tang.

They, however, show bigger increases when the economy rebounded.

Apartments and condominiums are comparatively flat.

Average rental yields:

- Condominiums: between 6% and 8%

- Terraced, semi-detached and bungalows: 2%-4% Shops: 6%-8%

- Retail lots: 4%-6%

- Office suites: 4%-6%

Financial considerations

Know your total cost and establish a realistic budget. Although some

developments allow buyers to go for 90% financing, this may not be wise in

spite of today's so-called low interest rate regime. A banker will tell you

at the end of X number of years, with an X amount of loan, the total

payments you would have made. The total amount paid would be generally about

twice the loan amount.

Instead of going for maximum financing, have a large down payment. At the

same time, go for a package that allows you to pay towards the loan

principal as and when you have the means, without incurring extra charges

when you do this. This helps to reduce interest payment. Most packages tie

down the borrower for between three to five years. There are some that do

not.